Most Founders Can't Afford Their Own Patterns. Mark Can.

In December 2012, Mark Zuckerberg sat with a small team at Facebook HQ and personally wrote code for a Snapchat clone. They built it in 12 days. He recorded the push-notification sound on his phone — "Poke" — as a joke, and it shipped. TechCrunch broke the story on December 21, 2012, including the detail that the CEO was coding despite saying publicly he rarely programmed anymore.

Poke lasted 14 months before Facebook quietly killed it.

That 12-day sprint is the Rosetta Stone for every decision Meta has made since. If you want to understand why a trillion-dollar company keeps producing the same kind of expensive mistake — and what that has to do with you as a founder — start with Poke and trace forward.

The pattern of one man, replayed at increasing scale

I spent weeks mapping every major Meta project, acquisition, and strategic move. The failures aren't random. They cluster into five specific behaviors by one specific person:

One: When a competitor refuses to sell, clone them fast.

Snapchat rejected a $3B offer in 2013. Meta's response, documented in unsealed FTC emails and court filings: Poke, Slingshot, Rooms, Riff, Lifestage, Bonfire — all targeting Snapchat's user base, all dead within two years. When clones didn't work, Meta built "Project Ghostbusters" — a 2016-2019 program using the Onavo VPN to run man-in-the-middle attacks on Snapchat, YouTube, and Amazon traffic, decrypting competitor analytics without user consent. Zuckerberg's own email, June 9, 2016, unsealed in court: direct request to "figure out a new way to get reliable analytics" on Snapchat.

His 2008 email, surfaced at the 2025 FTC antitrust trial, is cleaner: "It is better to buy than compete."

Two: When personal conviction forms, the company's strategy follows — with no counterweight.

In October 2021, Zuckerberg renamed Facebook to Meta on his own authority. At the Connect 2021 keynote he said on stage: "No one knows exactly which models are going to work and make this sustainable." That is a CEO publicly admitting the thesis isn't validated while announcing a corporate rebrand around it. Reality Labs lost $6.6B in 2020, $10.2B in 2021, $13.7B in 2022, $16.1B in 2023, $17.7B in 2024, $19.2B in 2025 — over $77B cumulatively. Horizon Worlds, the flagship, shut down in VR on March 31, 2026.

Oculus founder Palmer Luckey, on stage at the WSJ Tech Live conference, called it Mark's "project car" — an expensive personal hobby nobody else at the company could redirect.

Three: When attention moves, old priorities get starved.

Parse co-founder Ilya Sukhar, on Software Engineering Daily, described the lived experience: "Zuckerberg's strategy included only a few priorities every 6 months, then he just shuffled his people between those and became super focused on the next big thing while dropping everything else." Parse was a market-leading backend-as-a-service with 600,000 apps. Shut down in 2017. Ready at Dawn — closed in 2024, working on what its co-founder called "one of the most revolutionary VR games ever." Bloomberg's 2025 profile of Zuckerberg: "When he moves to a new big thing, plenty of the most loyal workers jump with him. Often when there's still plenty of work to be done, he's on to the next big thing."

Four: Money as a substitute for thesis.

$85M on Parse. $2B on Oculus. $19B on WhatsApp. $14.3B on Scale AI in June 2025. $77B on the metaverse. $140B on AI infrastructure in three years. $600B planned through 2028. Roughly $200B total burned on bets that haven't worked yet, with Meta still in 4th place on the AI intelligence index. Zuckerberg's own framing on the Dwarkesh Patel podcast (April 2024): "We basically realized we've got to solve general intelligence and we just upped the ante and the investment to make sure that we could do that." Up the ante. That's the strategy.

Five: Under pressure, take over operationally — and become the bottleneck.

Meta President Dina Powell McCormick, on stage at Semafor's World Economy Summit in April 2026: "Mark has actually moved his desk and is seated in the AI lab with Alex Wang and Nat Friedman, and he's coding all day long." She added, nervously joking: "On the one hand, they are sort of like, 'Oh great, more advice from you Mark, as you're coding.'"

The $14.3B executive Zuckerberg hired to fix AI — Alexandr Wang — was reported by the Financial Times in December 2025 to be privately describing Mark's micromanagement as "suffocating" and "slowing progress." 600 AI employees laid off. Multiple senior leadership departures. The model codenamed Avocado delayed three times because internal tests show it lagging Google, OpenAI, and Anthropic.

The company became the shape of the founder

Here's the part that matters. These aren't five separate flaws. They're five surface expressions of one dynamic:

Meta is the structural fingerprint of Mark Zuckerberg's cognitive patterns, at scale, with no one able to correct course.

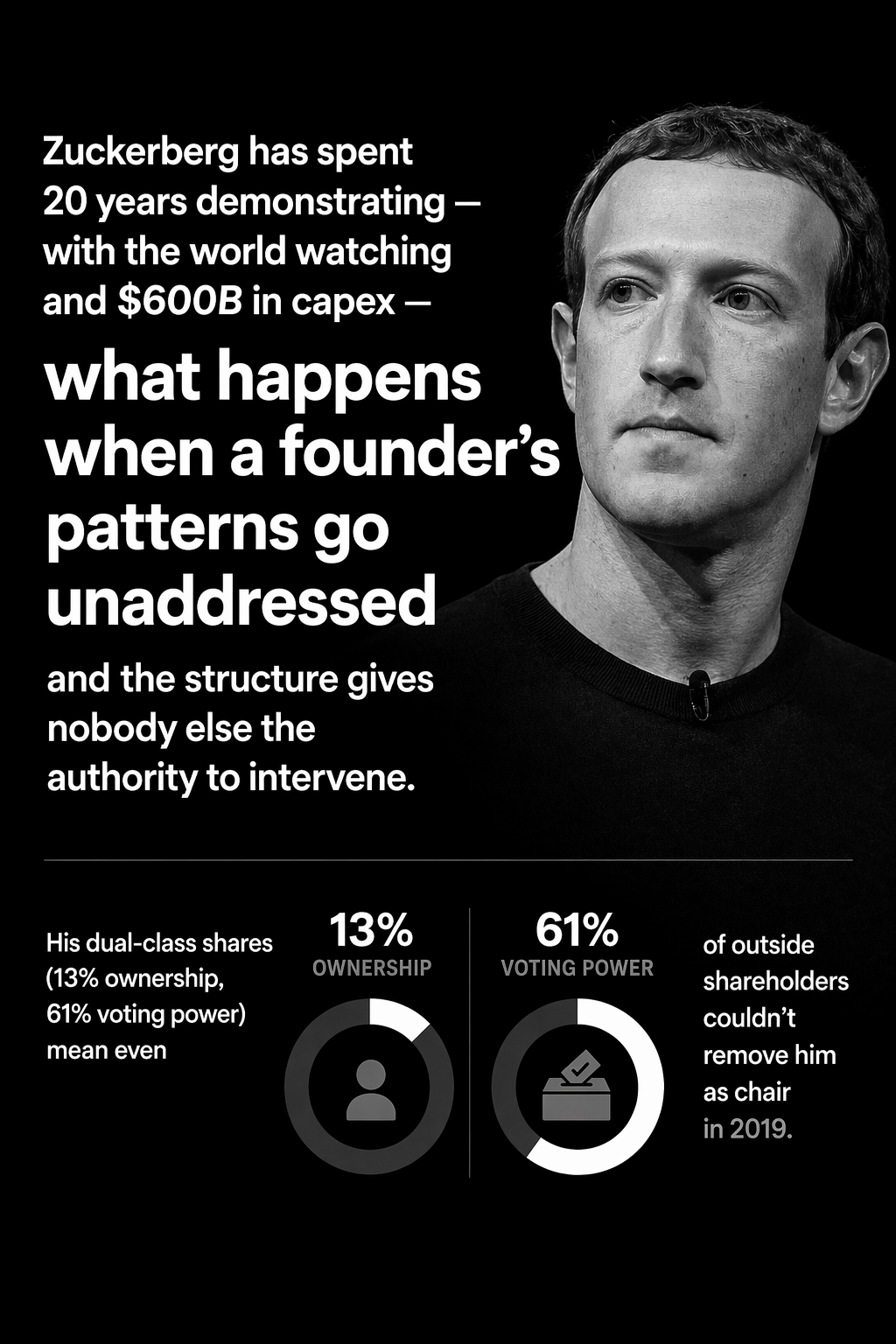

The dual-class share structure makes this literal. From Meta's own 10-K filing, published on SEC.gov: "[The] dual class common stock structure...provides Mark Zuckerberg, our founder, Chairman, and CEO, with the ability to control the outcome of matters requiring stockholder approval." He owns 13% of the company economically. He controls 61% of the votes. In 2019, 68% of outside shareholders voted to strip him of his chairmanship. His super-votes overrode them. In 2024, nearly 60% of non-insider shareholders voted to give the independent board chair authority to add agenda items Mark objected to. Mark objected. Proposal failed.

Meta's $201B of annual revenue, 97.6% of which is advertising, runs on top of this structure. Which means the operational truth of the company is: one man's patterns get executed at $200B/year of scale, financed by an ad business he bought or cloned 10+ years ago, with no institutional mechanism to stop him.

Why this actually matters for your company

You are not Mark Zuckerberg. That's the point.

Every founder I work with has patterns. A reactive reflex that fires when a competitor launches something new. A pet project they keep investing in past the point the market has signaled. A tendency to abandon the old thing the moment the next shiny opportunity appears. A habit of throwing money at problems that are actually thesis problems. A default to taking over and micromanaging when things go sideways.

The patterns themselves aren't the issue. Every operator has them. The issue is that Mark can afford to run his patterns for 20 years and absorb $200B+ in associated costs because Facebook and Instagram print ad cash. You probably can't.

When you run the reactive-cloning reflex with $2M in the bank, you don't lose a side project. You lose the company.

When you run the "upped the ante" pattern on your last $500K of runway, you don't get 18 months to course-correct. You get a bridge round that doesn't close.

When you run founder-mode micromanagement on the one senior hire you could afford, they don't stay "suffocating" quietly — they leave, and you have nobody to replace them.

This is the real cost of unchecked founder patterns. Most founders find out by running out of money.

The half-knowing is the dangerous part

Here's what I see across hundreds of founder conversations: most of you can almost see your patterns.

You half-know you avoid the conversations that would give you hard customer feedback. You half-know you keep pivoting before the last bet had time to compound. You half-know the reason your best hire left is you. You half-know that the framework you're currently obsessed with is the same shape as the last three frameworks you were obsessed with.

Half-knowing is enough to feel guilty. Not enough to operationalize.

Therapy helps with the personal layer — why you developed the pattern. It rarely produces a business-specific action plan. Advisors give opinions that land in the moment and dissolve by Tuesday. AI tools process whatever framing you give them, which means they confirm the lens that caused the problem.

What you need is a diagnostic that measures how you think, decide, and filter information — and then turns what you half-know into a specific set of actions you can start executing this week. Not a score. Not another framework. A bridge between what you're starting to see about yourself and what you actually do on Monday morning.

What Peak Genesis does

We built a free assessment — 50 minutes, 46 questions — that produces a scored PMF diagnostic covering every dimension of your business, including how your own patterns are shaping what gets built and what gets ignored. You get a PMF score, a risk grade, your top blind spots, and the 5 things to fix first, all grounded in evidence from your own words.

For most founders, this is enough to move from half-knowing to acting.

For those who want the full picture, the Full Diagnostic produces a 12-week execution plan with every action traced to a specific finding about how you operate — the bridge between "I suspect I'm the bottleneck" and "here's what I do about it Monday."

Mark can afford to run his patterns unchecked for another 20 years. He has a $201B ad business covering him. You have your runway.

The founders who make it to the other side aren't the ones without patterns. They're the ones who learned to see their patterns before the market showed them, expensively.

Find yours here: https://clarityonpmf.com

In December 2012, Mark Zuckerberg sat with a small team at Facebook HQ and personally wrote code for a Snapchat clone. They built it in 12 days. He recorded the push-notification sound on his phone — "Poke" — as a joke, and it shipped. TechCrunch broke the story on December 21, 2012, including the detail that the CEO was coding despite saying publicly he rarely programmed anymore.

Poke lasted 14 months before Facebook quietly killed it.

That 12-day sprint is the Rosetta Stone for every decision Meta has made since. If you want to understand why a trillion-dollar company keeps producing the same kind of expensive mistake — and what that has to do with you as a founder — start with Poke and trace forward.

The pattern of one man, replayed at increasing scale

I spent weeks mapping every major Meta project, acquisition, and strategic move. The failures aren't random. They cluster into five specific behaviors by one specific person:

One: When a competitor refuses to sell, clone them fast.

Snapchat rejected a $3B offer in 2013. Meta's response, documented in unsealed FTC emails and court filings: Poke, Slingshot, Rooms, Riff, Lifestage, Bonfire — all targeting Snapchat's user base, all dead within two years. When clones didn't work, Meta built "Project Ghostbusters" — a 2016-2019 program using the Onavo VPN to run man-in-the-middle attacks on Snapchat, YouTube, and Amazon traffic, decrypting competitor analytics without user consent. Zuckerberg's own email, June 9, 2016, unsealed in court: direct request to "figure out a new way to get reliable analytics" on Snapchat.

His 2008 email, surfaced at the 2025 FTC antitrust trial, is cleaner: "It is better to buy than compete."

Two: When personal conviction forms, the company's strategy follows — with no counterweight.

In October 2021, Zuckerberg renamed Facebook to Meta on his own authority. At the Connect 2021 keynote he said on stage: "No one knows exactly which models are going to work and make this sustainable." That is a CEO publicly admitting the thesis isn't validated while announcing a corporate rebrand around it. Reality Labs lost $6.6B in 2020, $10.2B in 2021, $13.7B in 2022, $16.1B in 2023, $17.7B in 2024, $19.2B in 2025 — over $77B cumulatively. Horizon Worlds, the flagship, shut down in VR on March 31, 2026.

Oculus founder Palmer Luckey, on stage at the WSJ Tech Live conference, called it Mark's "project car" — an expensive personal hobby nobody else at the company could redirect.

Three: When attention moves, old priorities get starved.

Parse co-founder Ilya Sukhar, on Software Engineering Daily, described the lived experience: "Zuckerberg's strategy included only a few priorities every 6 months, then he just shuffled his people between those and became super focused on the next big thing while dropping everything else." Parse was a market-leading backend-as-a-service with 600,000 apps. Shut down in 2017. Ready at Dawn — closed in 2024, working on what its co-founder called "one of the most revolutionary VR games ever." Bloomberg's 2025 profile of Zuckerberg: "When he moves to a new big thing, plenty of the most loyal workers jump with him. Often when there's still plenty of work to be done, he's on to the next big thing."

Four: Money as a substitute for thesis.

$85M on Parse. $2B on Oculus. $19B on WhatsApp. $14.3B on Scale AI in June 2025. $77B on the metaverse. $140B on AI infrastructure in three years. $600B planned through 2028. Roughly $200B total burned on bets that haven't worked yet, with Meta still in 4th place on the AI intelligence index. Zuckerberg's own framing on the Dwarkesh Patel podcast (April 2024): "We basically realized we've got to solve general intelligence and we just upped the ante and the investment to make sure that we could do that." Up the ante. That's the strategy.

Five: Under pressure, take over operationally — and become the bottleneck.

Meta President Dina Powell McCormick, on stage at Semafor's World Economy Summit in April 2026: "Mark has actually moved his desk and is seated in the AI lab with Alex Wang and Nat Friedman, and he's coding all day long." She added, nervously joking: "On the one hand, they are sort of like, 'Oh great, more advice from you Mark, as you're coding.'"

The $14.3B executive Zuckerberg hired to fix AI — Alexandr Wang — was reported by the Financial Times in December 2025 to be privately describing Mark's micromanagement as "suffocating" and "slowing progress." 600 AI employees laid off. Multiple senior leadership departures. The model codenamed Avocado delayed three times because internal tests show it lagging Google, OpenAI, and Anthropic.

The company became the shape of the founder

Here's the part that matters. These aren't five separate flaws. They're five surface expressions of one dynamic:

Meta is the structural fingerprint of Mark Zuckerberg's cognitive patterns, at scale, with no one able to correct course.

The dual-class share structure makes this literal. From Meta's own 10-K filing, published on SEC.gov: "[The] dual class common stock structure...provides Mark Zuckerberg, our founder, Chairman, and CEO, with the ability to control the outcome of matters requiring stockholder approval." He owns 13% of the company economically. He controls 61% of the votes. In 2019, 68% of outside shareholders voted to strip him of his chairmanship. His super-votes overrode them. In 2024, nearly 60% of non-insider shareholders voted to give the independent board chair authority to add agenda items Mark objected to. Mark objected. Proposal failed.

Meta's $201B of annual revenue, 97.6% of which is advertising, runs on top of this structure. Which means the operational truth of the company is: one man's patterns get executed at $200B/year of scale, financed by an ad business he bought or cloned 10+ years ago, with no institutional mechanism to stop him.

Why this actually matters for your company

You are not Mark Zuckerberg. That's the point.

Every founder I work with has patterns. A reactive reflex that fires when a competitor launches something new. A pet project they keep investing in past the point the market has signaled. A tendency to abandon the old thing the moment the next shiny opportunity appears. A habit of throwing money at problems that are actually thesis problems. A default to taking over and micromanaging when things go sideways.

The patterns themselves aren't the issue. Every operator has them. The issue is that Mark can afford to run his patterns for 20 years and absorb $200B+ in associated costs because Facebook and Instagram print ad cash. You probably can't.

When you run the reactive-cloning reflex with $2M in the bank, you don't lose a side project. You lose the company.

When you run the "upped the ante" pattern on your last $500K of runway, you don't get 18 months to course-correct. You get a bridge round that doesn't close.

When you run founder-mode micromanagement on the one senior hire you could afford, they don't stay "suffocating" quietly — they leave, and you have nobody to replace them.

This is the real cost of unchecked founder patterns. Most founders find out by running out of money.

The half-knowing is the dangerous part

Here's what I see across hundreds of founder conversations: most of you can almost see your patterns.

You half-know you avoid the conversations that would give you hard customer feedback. You half-know you keep pivoting before the last bet had time to compound. You half-know the reason your best hire left is you. You half-know that the framework you're currently obsessed with is the same shape as the last three frameworks you were obsessed with.

Half-knowing is enough to feel guilty. Not enough to operationalize.

Therapy helps with the personal layer — why you developed the pattern. It rarely produces a business-specific action plan. Advisors give opinions that land in the moment and dissolve by Tuesday. AI tools process whatever framing you give them, which means they confirm the lens that caused the problem.

What you need is a diagnostic that measures how you think, decide, and filter information — and then turns what you half-know into a specific set of actions you can start executing this week. Not a score. Not another framework. A bridge between what you're starting to see about yourself and what you actually do on Monday morning.

What Peak Genesis does

We built a free assessment — 50 minutes, 46 questions — that produces a scored PMF diagnostic covering every dimension of your business, including how your own patterns are shaping what gets built and what gets ignored. You get a PMF score, a risk grade, your top blind spots, and the 5 things to fix first, all grounded in evidence from your own words.

For most founders, this is enough to move from half-knowing to acting.

For those who want the full picture, the Full Diagnostic produces a 12-week execution plan with every action traced to a specific finding about how you operate — the bridge between "I suspect I'm the bottleneck" and "here's what I do about it Monday."

Mark can afford to run his patterns unchecked for another 20 years. He has a $201B ad business covering him. You have your runway.

The founders who make it to the other side aren't the ones without patterns. They're the ones who learned to see their patterns before the market showed them, expensively.

Find yours here: https://clarityonpmf.com